As promised last week, in this blog I am following up on the expansion of data centers into developing countries, with a focus on India. I am starting with a broad AI description (via Google).

Google AI Prompt: Data Centers in Developing Countries

Data centers are becoming a primary driver of foreign direct investment (FDI) in developing countries, with announced investments exceeding $270 billion in 2025 alone. This surge is fueled by the rapid expansion of AI and cloud computing, which requires massive infrastructure often built in emerging markets to reduce operational costs and meet growing local digital demand.

Key Growing Markets

The growth is concentrated in a few “hub” countries that offer strategic geographic advantages or supportive government policies:

India

: Projected to nearly double its capacity from 950 MW in 2024 to 1,800 MW by 2026. Major investments include Microsoft ($3 billion) and Yotta Data Services ($500 million).

Brazil

: The dominant leader in Latin America, hosting over 37% of the region’s data centers. It serves as a primary hub for South American digital traffic due to its stable urban infrastructure.

South Africa

: Africa’s most mature market, hosting roughly 100 data centers. Newer entrants like Equinix are investing hundreds of millions to expand Johannesburg’s capacity.

: Emerging as a critical “secondary” site for the US market, with significant development in Querétaro due to lower land costs and government incentives.

Primary Challenges

While data centers offer economic potential, they face severe structural and social hurdles in developing regions:

- Energy Grid Instability: Many nations struggle with “firm” power (steady, 24/7 supply). Data centers in

India and South Africa must often contend with regular outages or unstable grids.

- Resource Depletion: Large facilities consume massive amounts of water for cooling. In Mexico , local communities have protested against data centers during droughts, fearing they will drain drinking water supplies.

- Social & Environmental Pushback: There is growing resistance from local communities who feel the “digital gold rush” benefits foreign tech giants without providing long-term local prosperity or infrastructure improvements.

Strategic Solutions for Sustainable Growth

To balance demand with local needs, developers and governments are exploring new models:

- Renewable Energy Integration: Utilizing massive local resources like the

Grand Ethiopian Renaissance Dam

or Kenya’s geothermal reserves to power “green” data centers.

- Microgrids: Moving away from centralized grids toward solar-storage-gas microgrids to ensure stability without straining public utilities.

- Co-Investment Frameworks: Negotiating for more than just land; regions are asking for commitments to local R&D, workforce training, and energy innovation.

What fiscal incentives attract data center FDI in India or Brazil?

What are some examples of successful community data center partnerships in developing countries?

Focus on India

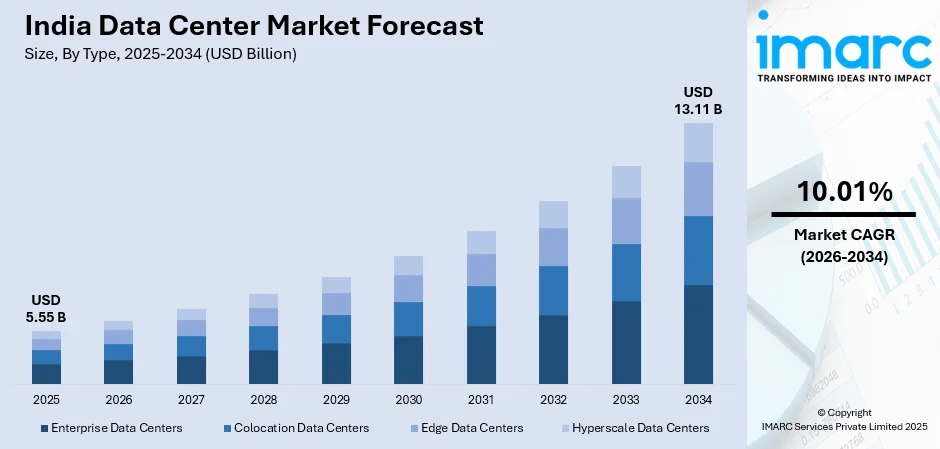

Figure 1 – India data center market forecast (Source: IMARC Group)

Figure 1 – India data center market forecast (Source: IMARC Group)

To understand Figure 1, we need some explanations about the different types of data centers. Again, I’m using AI (via Google):

AI data centers are specialized facilities designed for intensive computing workloads, primarily categorized by scale and deployment model. Key types include hyperscale (massive cloud infrastructure), colocation (rented, shared space), edge (localized for low latency), and enterprise/on-premises (private, company-owned), often employing specialized cooling.

- Hyperscale Data Centers:Vast, high-speed facilities owned by major cloud providers (e.g., AWS, GCP, Microsoft Azure) offering massive scale and efficient processing for training AI models.

- Colocation Data Centers:Facilities where enterprises lease space, power, and cooling to deploy their own AI hardware, offering high performance with lower upfront investment

- AI Edge Data Centers:Smaller centers placed near users or data sources to deliver fast, real-time AI inference and lower latency.

- Enterprise/On-Premises Data Centers:Private data centers managed in-house by an organization, providing total control and security, commonly used for specialized AI training.

- Modular Data Centers:Pre-fabricated, portable, and self-contained units ideal for rapid, temporary deployment or remote locations.

AI Data Center Characteristics:

-

High Power/Cooling:Designed for high-density, energy-intensive GPU setups.

-

Hybrid Models:Often combine on-premises security with cloud agility.

-

Specialized Infrastructure:Include high-speed networks (InfiniBand/Ethernet) and massive storage for data training.

In the News

Data Center Surge Reaches India as American Tech Giants Invest Billions (NYT)

Satya Nadella, Microsoft’s chief executive, was striding across a stage in New Delhi, extolling his company’s $17.5 billion investment in artificial intelligence and the benefits it would bring to his native country’s 1.4 billion people. While he was speaking, Amazon made a rival announcement, promising to throw $35 billion into A.I.-driven projects across India.

A flood of money for data centers, cloud computing and other hardware has come to India. Two months before the near-simultaneous Microsoft-Amazon announcements, Google committed $15 billion to data centers in partnerships with two of India’s biggest conglomerates, the Adani Group and Bharti Airtel.

That $67.5 billion, to be spent over the next five years, is just the crest of a wave. A fourth American tech giant, Meta, is having a plant built near Google’s, as are India’s other biggest industrial houses, Reliance and Tata.

“This is going to be one of the largest single-sector investments that India’s ever seen,” said Somnath Mukherjee, chief investment officer at ASK Wealth Advisors in Mumbai.

Report on the India Data Center Market (IMARC Group)

The India data center market size was valued at USD 5.55 Billion in 2025 and is projected to reach USD 13.11 Billion by 2034, growing at a compound annual growth rate of 10.01% from 2026-2034.

The market is driven by rapid digital transformation, increasing cloud adoption, and rising demand for data storage solutions across enterprises. Growing internet penetration and smartphone usage are fueling data generation, while government initiatives supporting digital infrastructure development are accelerating investments. The expansion of e-commerce, fintech, and streaming services further propels demand for robust data center facilities. Enhanced focus on data localization requirements and emerging technologies continues strengthening the India data center market share.

At the same time, as mentioned above, some are concerned about the amount of water and energy data centers consume:

More than a dozen investors are pressuring Amazon, Microsoft, and Alphabet’s Google to provide detailed data on water and energy consumption at their U.S. data centers, Reuters reported today. The pressure comes as all three companies have recently scrapped multibillion-dollar data center projects following community opposition, and as North American data centers consumed nearly 1 trillion liters of water in 2025, according to market research firm Mordor Intelligence.

To continue the conversation, I asked AI (via Google) “Why Google, Microsoft, Amazon and Apple are building Data Centers in India?” and it answered with the following:

Google, Microsoft, Amazon, and Apple are investing heavily in India’s data centers primarily to secure long-term tax benefits, comply with stricter data residency laws, and capitalize on a massive, unserved AI market. By building locally, they can offer lower latency to India’s nearly one billion internet users while establishing a strategic alternative to China.

- Significant Financial Incentives

- 20-Year Tax Holiday: The Indian Government recently announced a tax exemption until 2047 for foreign cloud providers that use India-based data centers to serve global customers.

- Infrastructure Status: India has granted data centers “infrastructure status,” which allows these companies to access credit at lower interest rates and simplifies land acquisition.

- Lower Operational Costs: Building and operating in India is significantly cheaper than in hubs like Singapore or London. For instance, industrial electricity in Hyderabad costs roughly 7 cents per kWh, compared to 18 cents in the U.S..

- Strict Data Localization Laws

- Sovereignty Mandates: Indian regulators now require that sensitive financial, health, and telecom data be stored physically within the country’s borders.

- Regulatory Compliance: The Digital Personal Data Protection (DPDP) Act of 2023 creates a strict legal framework that pushes companies to host data locally to ensure rapid law enforcement access and national security.

- The “AI Gold Rush” and Latency

- Bridging the Storage Gap: While India generates 20% of the world’s data, it currently only has about 3% of global storage capacity. This massive undersupply represents a major growth opportunity for hyperscalers like AWS and Microsoft.

- Performance: Localized servers are essential for modern AI and real-time applications. Hosting in India eliminates the latency delays previously caused by routing traffic through Singapore.

- Strategic Geopolitical Pivot

-

China Alternative: Rising trade tensions and regulatory hurdles in China have led U.S. tech giants to view India as the most viable, stable alternative for long-term AI and cloud infrastructure in Asia.

-

Talent Ecosystem: India’s massive pool of engineering talent provides a ready workforce to manage and innovate within these new facilities.

What this description is missing is the following:

Sundar Pichai (CEO of Google), Satya Nadella (CEO of Microsoft), Indra K. Nooyi (Ex CEO of Pepsi Cola and now director in Amazon), and Sabin Khan (Chief Operating Officer of Apple) were all born in India.

Cost and Public Acceptance are obviously also factors (analysis via Google AI):

Data centers in the US generally cost $600–$1,100 per square foot to build, with average costs per megawatt (MW) of IT load ranging from $7 million to $12 million. In India, construction costs are rising, with typical data center builds costing around ₹45–70 crore ($5.4M–$8.4M USD) per MW

The Cost of an Orbital Data Center (via Gemini):

The cost of building and operating an orbital (space-based) data center is significantly higher than its terrestrial counterparts, primarily due to the immense overhead of space logistics. As of 2026, industry estimates for a 1-gigawatt (GW) facility range from $42 billion to over $98 billion.

Breakdown of Major Costs

| Category | Estimated Cost (per GW) | Key Drivers |

| Capital Expenditure (CapEx) | $42B – $50B+ | Satellite construction, radiation-hardened hardware, and specialized AI chips. |

| Launch Costs | $10B+ | Heavy-lift requirements (e.g., SpaceX Starship) to move massive infrastructure into orbit. |

| Annual Operations (OpEx) | $8.8B – $14.7B |

I will continue to follow the expansion of AI into developing countries that do not enjoy the same advantages as India.

Pretty! This has been a really wonderful post. Many thanks for providing these details.