This blog will look at three issues related to the central role that data centers play in the start of phase II of global electrification, as was discussed in last week’s blog. I started last week’s blog with the following few lines:

Electrification requires an upgrade in order to power most of the post-WWII emerging global trends, which include the convergence of electrification, digitization, energy transition, nuclear threats, and security on a global scale! The main tool to accomplish such a gigantic role is data centers.

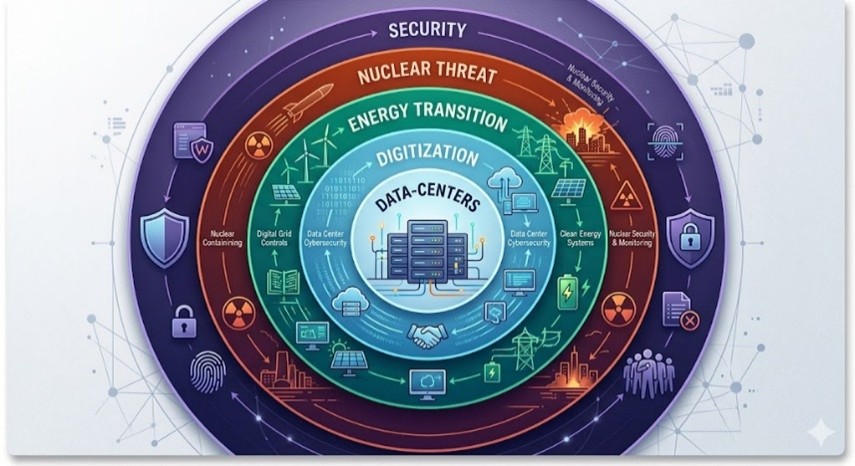

I have spoken a lot about a series of interconnected ongoing global trends. For this blog I asked AI (through Gemini):

Can you suggest a drawing of a modified Venn Diagram that consists of concentric circles with the inner one indicates data centers; surrounded by Digitization; Energy Transition; Nuclear Threat and Security?

Figure 1 (Generated by Gemini AI based on my prompt)

Figure 1 the first image I got as a response. I usually speak about these trends as a group of 6, but in this case, I have omitted the ongoing decrease in fertility. The reason is that in almost all cases, the decision of whether or not to have kids is still a private decision—one that rarely involves a consultation with AI. However, this might change.

As to the inclusion of nuclear threats and security in this co-dependence, it is enough to have a look at the present Iran-US-Israel war. Both the US and Israel have stated that the war is to prevent Iran from becoming a nuclear power. We can see the impacts that the war is having on the global economy, as I described in a previous blog (March 25, 2026), to be continued.

I asked AI (this time, Microsoft’s Copilot) about the duration of a “typical” data center agreement. This is what I got:

Environmental and Resource Mitigation Agreements

These are almost always tied to the active operation of the center.

- Duration: Perpetual (for as long as the facility is drawing power or water).

- Review Cycles: While the contract itself might not “end,” it often includes mandatory review periods (every 3 to 5 years) where the community can reassess noise levels or water usage to ensure the data center is still in compliance with modern standards.

Typical Timeline Summary

| Contract Type | Typical Duration | Renewal/Review |

| PILOT | 10–20 Years | Fixed term; requires new negotiation. |

| CBA | 20–30 Years | Often tied to the life of the building. |

| Host Agreement | 30 Years | Usually long-term stability. |

| Environmental | Ongoing/Operational | Periodic audits every 3–5 years. |

(CBA stands for Community Benefit Agreement)

I found the timing of these agreements interesting because the position of data centers, in their present form, is far from assured for the time period that the agreements commit to.

Meanwhile, there is a completely different technology that might shortly become valid competition for AI: quantum computing (see the October 8, 2024 blog). An MIT report from last summer gives an updated review of this technology:

Quantum computing is evolving into a tangible technology that holds significant business and commercial promise, although the exact timing of when it will impact those areas remains unclear, according to a new report led by researchers at the MIT Initiative on the Digital Economy. The “Quantum Index Report 2025” charts the technology’s momentum, with a comprehensive, data-driven assessment of the state of quantum technologies.

The inaugural report aims to make quantum computing and networking technologies more accessible to entrepreneurs, investors, teachers, and business decision makers — all of whom will play a critical role in how quantum computing is developed, commercialized, and governed.

“There are a lot of folks who are interested in what’s going on in quantum, but the field is impenetrable to them,” said Jonathan Ruane, a research scientist at MIT IDE and editor-in-chief of the “Quantum Index Report.” The report is co-authored by researchers Elif Kiesow and Johannes Galatsanos from MIT IDE, and Carl Dukatz, Edward Blomquist, and Prashant Shukla from Accenture.

IBM is one company at the forefront of this effort.

As I mentioned in last week’s blog, developing countries are now active participants in the electricity shift, including an increasing reliance on data centers. However, as my visualization in Figure 1 shows, data centers can play a key role in the security of a country. Many are asking the valid questions of how we can control and who is in charge of controlling this technology. This is not yet an issue for developing countries, as they don’t have the resources to be on their own. However, it is already an issue for rich, non-American (mainly European) countries, as The Economist article below shows:

A LOOK AT Europeans’ software budgets shows why they are worried about dependence on America. Germany’s federal government pays almost half a billion euros a year in license fees to Microsoft, an American software firm. A rough calculation by a French business association finds that large French companies buy more than $50bn in software and cloud services annually from Uncle Sam’s tech giants. Euro-zone imports of intellectual property services from America have ballooned to $200bn a year and counting (see chart). That is not surprising. Cloud and artificial-intelligence services could prove more transformative than online shopping, social media or internet search. And the four biggest American cloud and AI firms—Amazon, Google, Meta and Microsoft—are miles ahead of Europe. German politicians crow about a new €1bn ($1.16bn) data center near Munich; America’s big four invested over 350 times that in 2025 alone. Of almost 100 notable AI models released in the past year, according to Epoch AI, a research firm, only one was from the European Union. The grip of American tech is, if anything, growing tighter.

The last issue that will be addressed in this blog is the energy sources that present datacenters depend on. For this, I am referencing a Pew Research Center report from October of 2025, which that relies heavily on IEA (International Energy Administration) reporting:

How much energy do data centers use?

Total annual U.S. electricity consumption hit a record high in 2024, and that ceiling could rise if data centers continue expanding at their current pace.

U.S. data centers consumed 183 terawatt-hours (TWh) of electricity in 2024, according to IEA estimates. That works out to more than 4% of the country’s total electricity consumption last year – and is roughly equivalent to the annual electricity demand of the entire nation of Pakistan. By 2030, this figure is projected to grow by 133% to 426 TWh.

Because data centers handle many types of workloads, it’s difficult to distinguish the exact share of their total electricity demand that comes from AI alone. But a typical AI-focused hyperscaler annually consumes as much electricity as 100,000 households. The larger ones currently under construction are expected to use 20 times as much, the IEA predicts.

Since data centers are often geographically concentrated, they can significantly strain the power grids. In 2023, data centers consumed about 26% of the total electricity supply in Virginia and significant shares of the supply in North Dakota (15%), Nebraska (12%), Iowa (11%) and Oregon (11%), according to the Electric Power Research Institute.

What is energy used for at data centers?

Most of the electricity used by data centers – about 60% on average, the IEA reports – powers the servers that process and store digital information. This is especially true at AI-optimized hyperscale data centers, whose advanced servers are equipped with powerful computer chips that can perform trillions of mathematical calculations per second. These chips consume much more energy than their traditional counterparts, requiring two to four times as many watts to run.

The next-largest component of energy use at data centers are the cooling systems that prevent servers from overheating. This share ranges from about 7% at efficient hyperscalers to over 30% at less efficient enterprise facilities.

These cooling systems often require a large amount of water, though some types use more than others. In 2023, the country’s data centers directly consumed about 17 billion gallons of water – with hyperscale and colocation facilities using the lion’s share (84%) – according to estimates in a 2024 Berkeley Lab report commissioned by the U.S. Department of Energy. Hyperscale data centers alone are expected to consume between 16 billion and 33 billion gallons of water annually by 2028. (These figures exclude water consumed indirectly, such as in the process of electricity generation or semiconductor manufacturing.)

What are the main energy sources for data centers?

As of 2024, natural gas supplied over 40% of electricity for U.S. data centers, according to the IEA. Renewables such as wind and solar supplied about 24% of electricity at data centers, while nuclear power supplied around 20% and coal around 15%.

Natural gas is projected to continue supplying the largest share of energy at data centers through 2030, but nuclear power could eventually play a larger role. Several tech companies have recently announced purchasing agreements with nuclear power startups. Plans are also in the works to revive two retired nuclear power plants – Three Mile Island in Pennsylvania and Duane Arnold in Iowa – to meet growing energy demand from data centers.

Related: Support for expanding nuclear power is up in both parties since 2020

Several states – including California, Illinois, Minnesota, New Jersey and Virginia – have weighed bills requiring or incentivizing data centers to draw some of their power from renewable energy sources and to report their electricity and water usage.

The next blog will focus on the global water issues that are arising based on the new data centers’ water requirements.

The way this post separates data-center control from the energy sources underneath is helpful, because the diagrams and examples are easy to skim past without pausing on the assumptions. I often save stills from technical videos or recorded lectures when I need to compare charts side by side, and a simple Video Frame Extractor has become useful for that kind of review. It makes the hidden structure in a presentation easier to revisit later. Thanks for laying out the energy/control relationship so plainly.

I found your insights on the energy sources of data centers fascinating! With our growing reliance on technology, Geometry Dash Lite, how do you think we can balance efficiency with environmental responsibility?

Very well presented. Every quote was awesome and thanks for sharing the content. Keep sharing and keep motivating others.